Umbrella insurance, also called ‘excess liability’ insurance, is a type of catastrophic insurance which can protect your wealth up to the limitations of the policy coverage in the event that a civil judgment is made against you, specifically one for which there is insufficient or absent protection from existing insurance policies (e.g. homeowners, auto).

Why?

_____________

Gaps in Coverage

Your homeowners and auto insurance policies alone will not insulate your wealth from all forms of liability. There are numerous engagements and activities which do not fit neatly into the coverage of homeowners or auto insurance. Some examples for which an umbrella policy may provide protection include:

- Coverage for boat or jet ski rentals even if you don’t own a boat or have boat insurance.

- Coverage for short-term rentals of your property.

- Coverage for the actions of your children which are deemed ‘intentional’ rather than negligent.

Insufficient Coverage

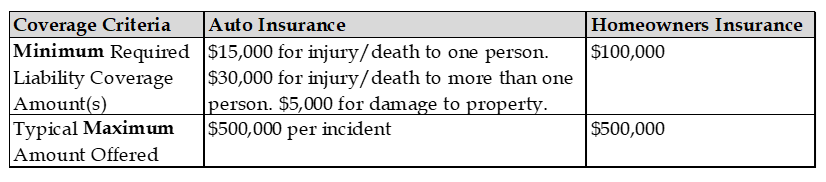

Most auto and homeowners policies provide insufficient protection in the event of a catastrophe.

How?

_____________

Add Coverage to Existing Auto and/or Homeowners Policy

Most insurers require an existing auto or property insurance policy that meets certain minimum coverage limits as a prerequisite for adding umbrella coverage to your policy (GEICO requires a minimum of $300,000 in bodily injury and $100,000 in property damage coverage on your auto policy, as well as $300,000 in homeowners or renters personal liability coverage. Allstate requires $300,000 in coverage per occurrence for primary and secondary residences, and $250,000 in bodily injury coverage per person for automobiles and motor homes).

Seek Out an Independent Broker

If your existing auto or property policy will not offer a satisfactory umbrella policy, independent insurance brokers can potentially find a policy from an insurance company that can fit your needs. There are quite a lot of insurance brokers out there, if you need assistance reach out to Pacific Wealth Management and we can connect you with someone that can help.

How Much?

_____________

Determining the Right Amount of Coverage

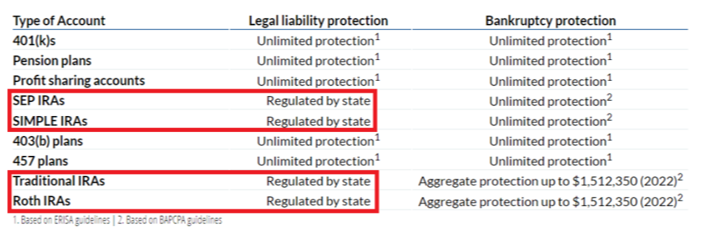

Generally, acquiring protection equal to the value of your net worth is advisable. Could you do with less? Technically, yes. Some types of retirement plans are fully protected from creditors, some are not. Importantly, California law does not provide a specific statutory protection for any form of IRA from non-bankruptcy creditors. California courts have determined that if a debtor will have available other moneys with which to fund retirement, those other moneys effectively offset to a like degree the protection for any IRA that the debtor may hold.[i]

If some plans are protected, why should they still be included in the calculation of the umbrella coverage policy amount? Because the protection of these funds is only statutorily guaranteed so long as they remain in the account. That means that if these accounts are ever rolled into a non-protected account (e.g. an IRA or Roth IRA), protection ceases. If funds in a protected account are distributed to a checking or savings account, you may be called upon by creditors to provide proof regarding the origin source of the funds. Inadequate documentation may put the value of these funds at risk.

Cost of Coverage

Umbrella policies typically start at $1 million in liability coverage for which the average cost of coverage is $383 per year for an individual with one home, two cars, and two drivers. The cost will typically increase by $75 or more for every $1 million in coverage.[ii]

[i] https://www.progressive.com/answers/umbrella-insurance-cost/

[ii] https://www.forbes.com/sites/jayadkisson/2022/02/07/is-your-california-ira-protected-from-creditors-probably-not/?sh=4d1f322955a6