The ‘One Big Beautiful Bill Act’ has meaningfully increased the potential for proprietors of short-term rental properties to significantly reduce their taxable income through 100% bonus depreciation.

The Unique Tax Advantage of Short-Term Rentals

_____________

Active vs. Passive Income

Unlike long-term rentals, income from rentals of properties with more than half of total rental days being for guest stays of less than 30 days, (such as an Airbnb or VBRO-listed units), is not considered ‘passive income’ by the IRS. While the operating losses of long-term rentals - such as from an annually leased property, cannot be deducted from other sources of income, by contrast- the operating losses of short-term rentals can be deducted against other sources of income- including that from your primary employment.

100% Bonus Depreciation and Operating Losses

The enshrinement of 100% bonus depreciation into law on a permanent basis unlocks the potential to plan qualifying improvements to short-term rental properties in such a way that taxable income can be meaningfully reduced. Because operating losses of short-term rentals are deductible against other sources of income, capital expenditures on qualifying improvements can be consolidated to pair with high income years for maximal tax-saving effect.

Standard or ‘straight-line’ depreciation spreads the expensing of an asset over an IRS-defined period depending on the type of asset being expensed. In the case of residential real estate, this could result in certain expenses in year 1 being booked against income for up to the following 27.5 years! Bonus depreciation, now set at 100% for qualified improvement allows you to deduct a the entirety of that cost in the first year the asset is placed in service.

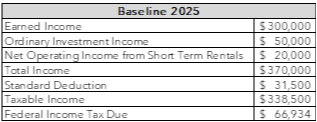

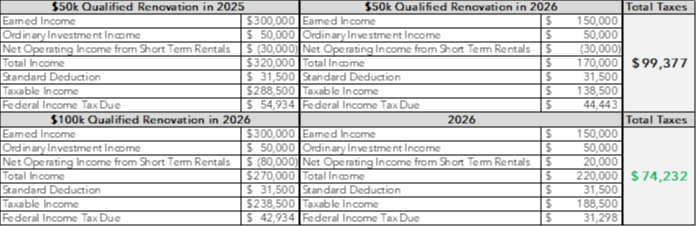

Consider the following scenario. A married couple filing jointly, who own and operate a short-term rental business which consistently generates $20,000 in annual net operating income. There are $100,000 of qualified improvements they wish to make. Their earned income will be significantly lower 2026 than in 2025.

If rather than spreading the expense outlay over two years at $50,000/yr., they consolidated the expenses to tax year 2025- a year in which their income is significantly higher than the year following- they can save over $25,000 in Federal taxes.

The combination of the ability to deduct 100% of the expenses of qualified improvements in the year in which they are placed in service (bonus depreciation), rather than over the course of up to potentially decades and to use resulting operating losses against other sources of income provides a unique wealth-generating opportunity.

The Ground Rules

_____________

Qualifying as ‘Active’

Short-term rentals, unlike long-term rentals, can be classified as an active trade or business for tax purposes if they meet specific IRS criteria and material participation requirements. These are:

- 7-Day Rule – The average rental period must be 7 days or less per booking.

- Material Participation – Owners must actively be involved in managing the property (e.g., direct booking, maintenance oversight, guest interactions).

- Perform all of the activities for the short-term rental business

- Spend more than 100 hours on short-term rental business, and no other person spends more than the owner

- Spend more than 500 hours on the short-term rental business

- Significant participation activities exceeding 100 hours and the owner’s total participation exceeds 500 hours

- Participating in the short-term rental business on the property for 5 of the previous 10 years

- Providing personal service or non-income producing activities for 3 of the previous years

If owners do not qualify based on the first 6 tests, regularly participating on a continuous basis during the year for at least 100 hours a year may also qualify.[1]

Expenses

The "One Big Beautiful Bill Act" permanently restores 100% bonus depreciation for qualifying rental property assets placed in service after January 19, 2025. This allows landlords to immediately deduct the full cost of many improvements and assets with a recovery period of 20 years or less.

To qualify under IRS Section 168(k), assets must:

- Be used in a trade or business- such as a short-term rental business in which you materially participate.

- Have a useful life of 20 years or less (consult IRS Publication 946 (2024))

- Must be placed-in-service (which means installed and ready for guests to use) in the same tax year you’re claiming the deduction.

Assets typically qualify for 100% bonus depreciation in 2025 and beyond include:

- Furniture

- Beds

- Sofas

- Dining sets

- Nightstands

- Outdoor furniture

- Appliances

- Dishwashers

- Dryers

- Stoves

- Refrigerators

- Electronics

- TVs

- Security systems

- Routers

- Smart home devices

- Fixtures and finishes

- New flooring

- Light fixtures

- Cabinetry

- Countertops

- Installation and delivery costs

- If directly tied to eligible assets

- Qualified Improvement Property (QIP)

- Interior, non-structural upgrades made to an existing building already placed in service—such as painting, drywall repair, or HVAC systems.

Disclaimer

_____________

Consult your CPA and Perform a Cost Segregation Study

Residential cost segregation involves identifying various property components that you can reclassify for 100% bonus depreciation. It is highly advised to consult with your CPA or qualified consultant to verify which planned improvements will qualify. Always seek counsel from a qualified financial planner to determine how such a strategy may be beneficial to your unique situation.

[1] https://www.kbkg.com/feature/unlock-active-income-by-offsetting-with-short-term-rentals