"Birthdays are good for you. Statistics show that the people with the most live the longest" — Larry Lorenzoni

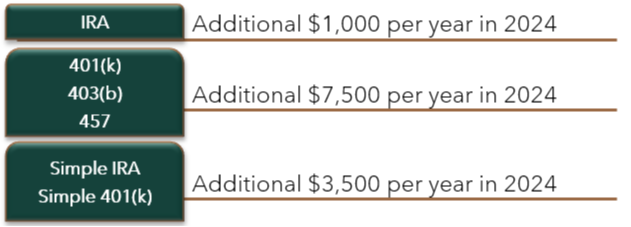

Age 50

Individuals who are 50 and older are allowed to make additional “catch-up” contributions to the following accounts:

Age 55

Are you leaving a position (voluntarily or involuntarily) in or after the year you turn 55? The rule of 55 allows for penalty-free withdrawals from a current employer's retirement plan in or after the calendar year you turn age 55. This is an exception to the IRS rule that normally levies a 10% penalty on withdrawals from employer-sponsored retirement plans before age 59½. Note that distributions from pre-tax retirement accounts are still taxed as ordinary income under the rule of 55.

Age 59 ½

Turning 59 ½ allows you to take penalty-free distributions from your retirement accounts. You will no longer be charged a 10% penalty on your distributions. Note that distributions from pre-tax traditional IRAs, 401(k) plans, and other employer-sponsored retirement plans are taxed as ordinary income.

Age 62

At the age of 62 workers can begin drawing Social Security retirement benefits. Be aware that your benefits will be permanently reduced should you choose to draw before your full retirement age. Ultimately, deciding on when to take your social security benefits can have a large impact on your financial plan. This decision should be examined on a case-by-case basis, and doing what your neighbor or golfing buddy did is not the best approach for such an important decision. The social security planning we do for our clients is what we call situational social security planning.

For more on this topic, please see this article When Do I Take My Social Security Benefit?

Age 65

You are now eligible for Medicare! The Social Security Administration advises applying for Medicare three months before turning 65. You’re first eligible to sign up for Part A and Part B during this period. If you’re already receiving Social Security benefits, you might be automatically enrolled in both parts, but it’s best to confirm this. If you don’t apply for Medicare during your enrollment period, you may be subject to a penalty that could stick around for years. If you are still working, contact your HR department to coordinate with your existing health insurance plan.

Age 65-67

Depending on the year you were born you are going to reach your full retirement age (FRA) sometime between 65 and 67. Once you have reached your FRA you are eligible to receive your full retirement benefit from Social Security. For instance, those born in 1955 can access their full benefits at the age of 66 years and 2 months. However, for those born in 1960 or later, they must wait until they turn 67 to receive their full benefit. If you have reached your FRA and plan on delaying, you will begin to accumulate delayed retirement credits (DRCs). DRCs will increase your Social Security benefits by a percentage each month that benefits are delayed past full retirement age, up to age 70.

Age 70

The last social security milestone is age 70. If you have made it this far without claiming your benefits you are in an exclusive club. Less than 10% of applications are filed by recipients age 70 or older[1]. It is time to apply for your beefed-up benefits. The Social Security Administration won't automatically send you your benefits, you will need to file your application for your benefits to begin.

Age 73

At the age of 73, you must begin taking your required minimum distributions (RMDs). RMDs are the minimum amounts you must withdraw from your retirement accounts each year. Generally, you must start taking withdrawals from your traditional IRA, SEP IRA, SIMPLE IRA, and other retirement plan accounts when you reach age 73. However, if you are still working, account owners in a workplace retirement plan (for example, 401(k) or profit-sharing plan) can delay taking their RMDs until the year they retire, unless they're a 5% owner of the business sponsoring the plan.

Remember if you are required to take an RMD and fail to withdraw the full amount of the RMD due for the year you will be penalized. Although the penalties have been reduced in recent years thanks to the Secure Act 2.0, it's best to avoid them altogether. The SECURE 2.0 Act drops the penalty, which is technically called an “excise tax” to 25%; possibly 10% if the RMD is timely corrected within two years[2]. The penalty is applied to your remaining outstanding RMD due for the year.

In conclusion, the journey towards retirement is marked by several significant milestones, each with its own set of opportunities and challenges. As we navigate through these important birthdays, it is crucial to stay informed and make strategic decisions that align with our retirement goals.

Remember, every individual’s situation is unique, and what works best for one may not work for another.

[1]https://www.ssa.gov/policy/docs/statcomps/supplement/2023/6b.html#table6.b5.1 (accessed March 21, 2024)

[2]https://www.ssa.gov/policy/docs/statcomps/supplement/2023/6b.html#table6.b5.1 (accessed March 21, 2024)