With the average price of a new vehicle now exceeding $50,000, understanding how much car you can truly afford is critical. This paper explores practical strategies and financial guidelines, like the 20/4/10 rule, to help buyers make informed decisions that align with their long-term financial goals.

How much car can you afford?

_____________

The Current Market

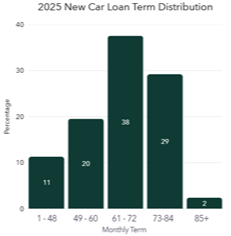

The average price of a new vehicle surpassed $50,000 in September, setting a new record high. As you would expect, as prices continue to climb, monthly payments for a car loan are rising as well. According to Experian’s Q1 2025 Automotive Finance Report, the average monthly payment for a new car reached $745 per month[1]. To accommodate these rising prices, consumers have been turning to longer-term loans, with 72-month and 84-month terms becoming increasingly common each year.

Are Cars Expensive or Feature Rich?

"Price is what you pay. Value is what you get.” – Warren Buffett

Modern vehicles come equipped with more technology, convenience, and safety features than ever before. New cars today often include 360-degree cameras, adaptive cruise control, heated and ventilated seats, wireless smartphone integration, and even semi-autonomous or full self-driving capabilities. While inflation contributes to higher vehicle prices, much of the increase is from these added functionalities and design improvements that have become standard in many new models.

It is important to note that the average price represents the mean cost of all new vehicles, not the price of the run-of-the-mill “average” family sedan. This figure includes everything from entry-level cars to luxury models and larger body styles such as trucks and SUVs. These higher-priced vehicles have a significant influence on the data, pulling the average up. However, it is reasonable for these models to be included, as consumer preferences have shifted. Also, buyers today increasingly choose trucks and SUVs over sedans and coupes.

Have a Plan Before You Buy

Whether or not you think they are expensive or appropriately priced, you need to have a plan in place before you visit the dealership to “just look” at new vehicles. Remember, dealerships do not have a fiduciary duty to you. Their goal is to close a sale, not to assess how the purchase fits into your overall financial picture. Salespeople are trained to keep you engaged until a deal is completed. Avoid discussing your total budget or how much you can afford to pay each month.

Guidelines

_____________

#1 An “All Cash” Offer

If you can afford to, paying for your vehicle in cash is the most financially sound approach. This approach eliminates the need for a loan, the associated monthly payments, and interest charges. Monthly payments can obscure the true cost of ownership, making expensive purchases seem affordable. By focusing on the total purchase price rather than the monthly payment, you maintain a clear view of the real cost and avoid unnecessary debt.

#2 The 20/4/10 Rule

The 20/4/10 rule is a rule of thumb for determining how much car you can afford. It provides a balanced framework for budgeting, borrowing, and maintaining long-term financial stability.

20% Down Payment

Make a down payment of at least 20% based on the total out-the-door cost of the vehicle, not just the manufacturer’s suggested retail price. This includes dealer fees, taxes, and add-ons.

Once you agree to purchase the vehicle, the salesperson will take you to the dealership's financing office. The financing office is where dealerships substantially improve their profit margins by upselling add-ons, things like aftermarket alarms, upgraded floor mats, and extended warranties. If you choose to include any of these extras, it’s important to calculate your 20% down payment based on the new out-the-door cost.

4 Year Loan Term (48 Months)

As the extended six-year or seven-year loans become more popular, buyers often end up purchasing more car than they can comfortably afford. Shorter loan terms reduce the total interest paid and, in turn, let you pay off the vehicle faster, freeing you from long-term payments. For flexibility, consider a five-year loan while making payments based on a four-year schedule. This method maintains financial discipline and sticks to the rule, while allowing room to reduce your monthly expenditures when cash flow is tight.

- The loan term trap

Dealers often ask potential buyers how much they can afford to pay each month and then extend the loan term to fit that number. This tactic can make the payment seem manageable. Having the 20/4/10 rule in mind when entering the dealership helps you stay focused on what you can truly afford rather than what appears affordable on a monthly basis. Some salespeople even break the cost down to the day, which is a sales trick.

“It’s only $24 a day. You almost spend that on lunch every day.”

Ten Percent of Gross Monthly Income

Your total vehicle expenses, including loan payments, insurance, and maintenance, should not exceed ten percent of your gross monthly income.

For most households, vehicles are the second largest expense after housing. Maintaining this ratio helps protect your financial goals and keeps your financial ratios in check. The goal is to prevent overspending. By staying at or below the ten-percent mark, you can use your excess cash flow to invest in appreciating assets rather than depreciating assets and avoid the risk of becoming “car poor.”

Running The Purchase Through Your Financial Plan

While the 20/4/10 rule is a strong starting point, every individual’s financial situation is different. At Pacific Wealth Management, we use this rule in combination with detailed financial planning tools to help clients determine:

- How much can they comfortably afford?

- How that purchase impacts their overall financial plan and long-term goals

We believe clients should enjoy the rewards of their hard work while remaining mindful of how major purchases affect their future. Thoughtful financial decisions today can help preserve flexibility, security, and peace of mind for tomorrow.

Frequently Asked Questions

What percentage of my income should I spend on a car?

A common rule of thumb is to limit the car payment to around 10% of your gross monthly income.

How big of a down payment should I make on a new car?

A larger down payment means you borrow less, leading to lower payments and less interest. We suggest putting down 20% (or more) to avoid being “upside down” on your loan (owing more than the car is worth).

How long should my car loan term be?

We suggest a maximum term of 48 months (four years). Shorter terms significantly reduce the total interest you pay and minimize the risk of being "upside down" on your loan, which is when you owe more than the car is worth. If cash flow is a concern, finance the car for 60 months, but commit to making payments based on a 48-month schedule to build in flexibility without sacrificing your long-term savings.

What is the 20/4/10 Rule?

This is a conservative guideline used to determine a financially healthy car budget. There are three requirements: make a 20% down payment, finance the purchase for a maximum of 4 years, and ensure that all vehicle-related expenses do not exceed 10% of your gross monthly income.

What car can I afford if I make $150,000 per year?

Based on the 20/4/10 Rule, your $150,000 annual income yields a gross monthly income of $12,500. This sets your total car budget limit (payment, insurance, and gas) at $1,250 per month. This monthly maximum supports a 4-year loan and 20% down payment for a total vehicle purchase price in the $54,000 to $57,500 range.

[1] Brozic, J. (2025, June 20). Average car payment in 2025. https://www.experian.com/blogs/ask-experian/average-car-payment/